[ad_1]

Regardless of quite a few acquisitions, the cell robotic market is actually not consolidating, and extra corporations pop up annually.

|

Hearken to this text  |

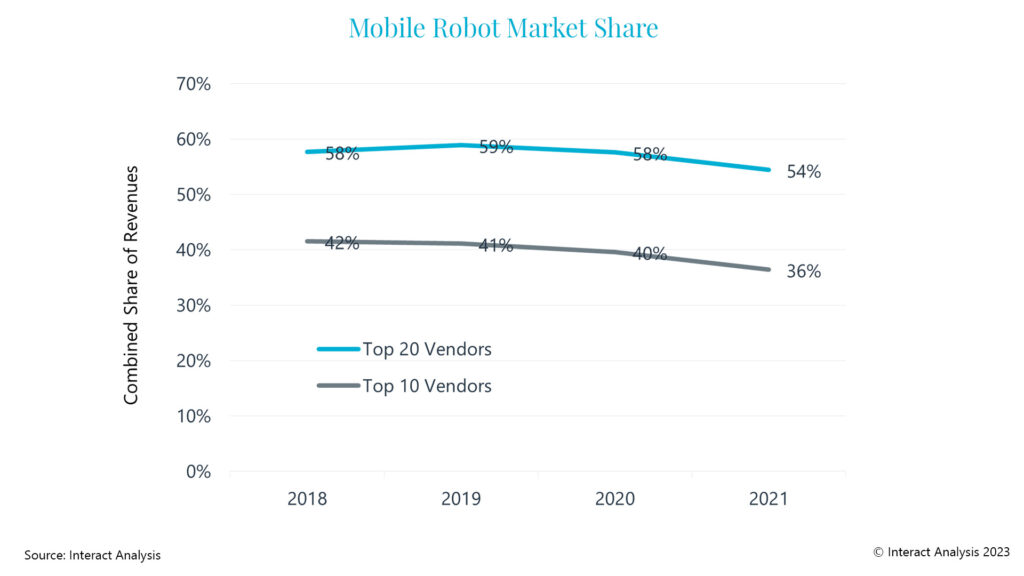

Regardless of quite a few acquisitions, the mobile robot market is actually not consolidating. Extra distributors emerge annually and extra industrial corporations are launching AMRs. The mixed market share of the highest 10 and high 20 main distributors barely modified between 2018 and 2020 and certainly dropped in 2021. Over the previous six years of researching this trade, we persistently establish new gamers (each start-ups and current corporations from adjoining markets that now supply AMRs).

Fragmentation

Given the dramatic progress charges and large variance in regional and vertical trade efficiency, additional fragmentation of the provider base appears doubtless – particularly when contemplating the big variety of present distributors and the continuous emergence of recent ones. As proven within the determine beneath, the highest 10 distributors of cell robots, captured simply 36% of complete trade revenues in 2021. Examine this to the extra mature industrial robotic market and there the highest 10 distributors take pleasure in a 73% mixed market share. The identical determine for collaborative robotic arms is even increased, at practically 85%.

Begin-Ups Develop Up

Most of the AMR start-ups from yester-year at the moment are producing important revenues (>$20m) having efficiently expanded on pilots performed in earlier years. US-based Locus Robotics turned the trade’s first “unicorn” being valued at over $1bn following its $150m fund-raising round close to two years ago. Chinese language rival, Geek+ has lengthy been rumored to be planning its IPO (maybe when trade and macro circumstances enhance), additional highlighting how far these once-start-ups have come.

The marginally extra established gamers have additionally seen their companies develop to the subsequent stage. Having significantly expanded their buyer and distribution bases, they’re benefiting from clients putting in bigger numbers of AMRs because the know-how turns into extra confirmed.

Vendor Efficiency Varies Vastly

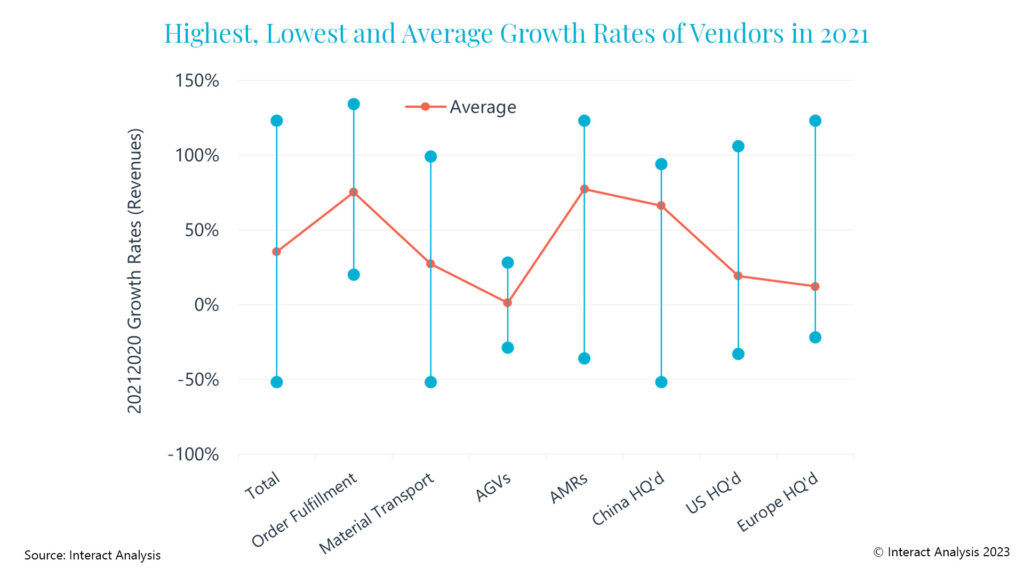

A part of the explanation that the trade shouldn’t be but consolidating is the truth that “cell automation” captures a large number of robotic sorts, industries and purposes. From automated tugger trains on automotive manufacturing traces, via to cell manipulators selecting particular person objects in a achievement middle. As such, vendor efficiency varies massively, and infrequently has little to do with their technique, product or efficiency however extra to do with driving the waves of their trade sector.

General income progress charges for distributors ranged from ~150% to adverse 50% in 2021. How a vendor carried out was largely linked to the principle finish industries and areas they had been uncovered to in addition to the kind(s) of cell robotic they provide.

What does the Future Maintain?

Main trade consolidation seems unlikely within the subsequent 2-3 years. Nonetheless, given the present financial surroundings and curiosity in cell automation, it’s doubtless a few of the smaller gamers will attempt to ‘money of their chips’. On the similar time, we’re additionally more likely to see much more distributors emerge over the approaching years. The online consequence will doubtless be neither consolidation nor additional fragmentation.

Some excessive profile and main AMR distributors have been acquired previously two years (notably Fetch Robotics and ASTI Cell Robotics). Nonetheless, each had been acquired by corporations with out an current cell robotic portfolio, so this didn’t assist consolidate or focus market revenues. There have been examples of cell robotic corporations buying each other. In September 2021, Locus Robotics acquired Waypoint Robotics. And late final 12 months Teradyne introduced the merger of its two cell robotic acquisitions (MiR and AutoGuide). At first look, this will likely point out market consolidation, however on nearer inspection, it reveals this M&A exercise was considerably insignificant as AutoGuide and Waypoint mixed accounted for lower than 1% of complete trade revenues on the level of acquisition.

Future acquisitions look doubtless, notably from industrial corporations wishing to capitalize on the excessive progress and margins seen within the cell automation sector. Nonetheless, our expectation is that this may come from corporations not already energetic inside the sector.

Different potential consumers could possibly be retailers or logistics corporations (a lá Amazon/Kiva) or bigger warehouse automation system integrators (the likes of Dematic or Honeywell Intelligrated). However in our opinion that appears unlikely and unwise presently. With so many alternative cell robotic distributors and applied sciences on the market, buying a single AMR firm right now brings little worth and places all their eggs in a single basket. As a substitute, it might be much better for a retailer or logistics firm to have the ability to purchase from a number of robotic corporations, selecting the best-in-breed for the duty at hand. Related for a system integrator, it might be way more compelling to have the ability to supply its clients the know-how from a number of robotic distributors (assuming they’ll get distribution agreements) relatively than from a single one it had acquired.

In fact, having the ability to benefit from utilizing AMR applied sciences from a number of distributors does include its personal challenges – most notably blended fleet orchestration. But that is another topic entirely!

Editor’s Observe: This story was initially printed by Interact Analysis and was reprinted with permission.

[ad_2]

Source link